The financial sector in Saudi Arabia is undergoing rapid growth as a result of Vision 2030. Banks are growing, fintech companies are growing, but with growth comes a need for compliance with SAMA regulations. If you are providing a digital wallet, loan service, or banking platform, SAMA compliance is critical.

Staying compliant safeguards your company, prevents penalties, and fosters customer confidence. This blog post will cover the function of SAMA, the licensing procedures, common compliance issues, and recommended approaches. We’ll also demonstrate how firms like Qualysec assist with your ongoing security and compliance needs.

SAMA’s Regulatory Role in Finance

SAMA (Saudi Central Bank) is the primary financial regulator for banks and fintech companies in Saudi Arabia. It grants licenses, sets policies, and makes sure financial operations are secure and safeguard clients.

SAMA also collaborates with other regulators like SDAIA (data/privacy), ZATCA (tax-related), and CMA (investment platforms). Each fintech or bank must comply with the unique rules that correspond with their business model and operations.

For fintech companies, SAMA also has a Regulatory Sandbox; this is a safe environment for testing and launching new products under regulation. This approach has led to the development of many startups with limited risk while also providing some level of compliance.

Read our latest insights on Cybersecurity in FinTech.

Licensing & Entry Requirements

If you want to operate as a bank or fintech in Saudi Arabia, you’ll need to get a license from SAMA (Saudi Central Bank). It does not matter if you are a new fintech company or an international financial services company looking to enter the Saudi market; SAMA applies the same conditions to every company that wants to establish itself with a license and expects companies to comply with regulatory and operational requirements before launching in the market.

Generally, there are two major approaches to entering the market:

1. SAMA Regulatory Sandbox – Fintechs can apply for SAMA’s Sandbox to have the opportunity to test innovative solutions under SAMA and then apply for a full license.

2. Full License – After the solution has been tested and proven to be secure and compliant, a full license is required to scale.

To get a license, you need to submit a business plan with:

1. Adequate minimum capital;

2. Credible management team; and

3. Technical documentation, especially regarding cybersecurity risk management, and customer protections.

Additionally, the companies must be fully prepared to provide KYC/AML procedures, data privacy policy, IT infrastructure, and internal controls. The application is reviewed carefully, and SAMA has the authority to request clarifications or seek amendments, etc., during the review.

The time it may take for SAMA to review a license will depend on the business model and availability of documentation, but on average, most reviews take a few months. While SAMA is stringent, they are very encouraging if they can establish transparency and prompt actions.

Common Compliance Challenge

Numerous banks and fintechs operating in Saudi Arabia struggle to achieve compliance with SAMA’s compliance obligations, especially during the onboarding phase. One particular area of challenge is understanding and applying SAMA’s Cybersecurity Framework. Several firms lack a strong internal security setup, which increases their vulnerability and results in insufficient documentation during reviews.

Also, AML (Anti-Money Laundering) and KYC (Know Your Customer) compliance are frequently problematic. SAMA requires firms to have automated systems to monitor for suspicious transactions, as well as identity verification for customers. Startups, primarily, struggle to create or properly integrate those systems into their onboarding and client activity processes.

Data privacy and security are also crucial. With the arrival of SDAIA and PDPL regulations, companies now have to guarantee they manage, share, and store customer data in a secure and compliant way. Non-compliance or lack of understanding can lead to fines or setbacks in getting the necessary license.

Lastly, regulatory updates are extremely important. SAMA often publishes and issues new circulars and updates that organisations need to follow. Underestimating this and not being aware of everything releases you from compliance. Staying abreast of the happenings, ensuring the internal controls are clear, and having experts guide you through it can ultimately alleviate much of this burden.

Stay updated with our latest insights on Penetration Testing Compliance.

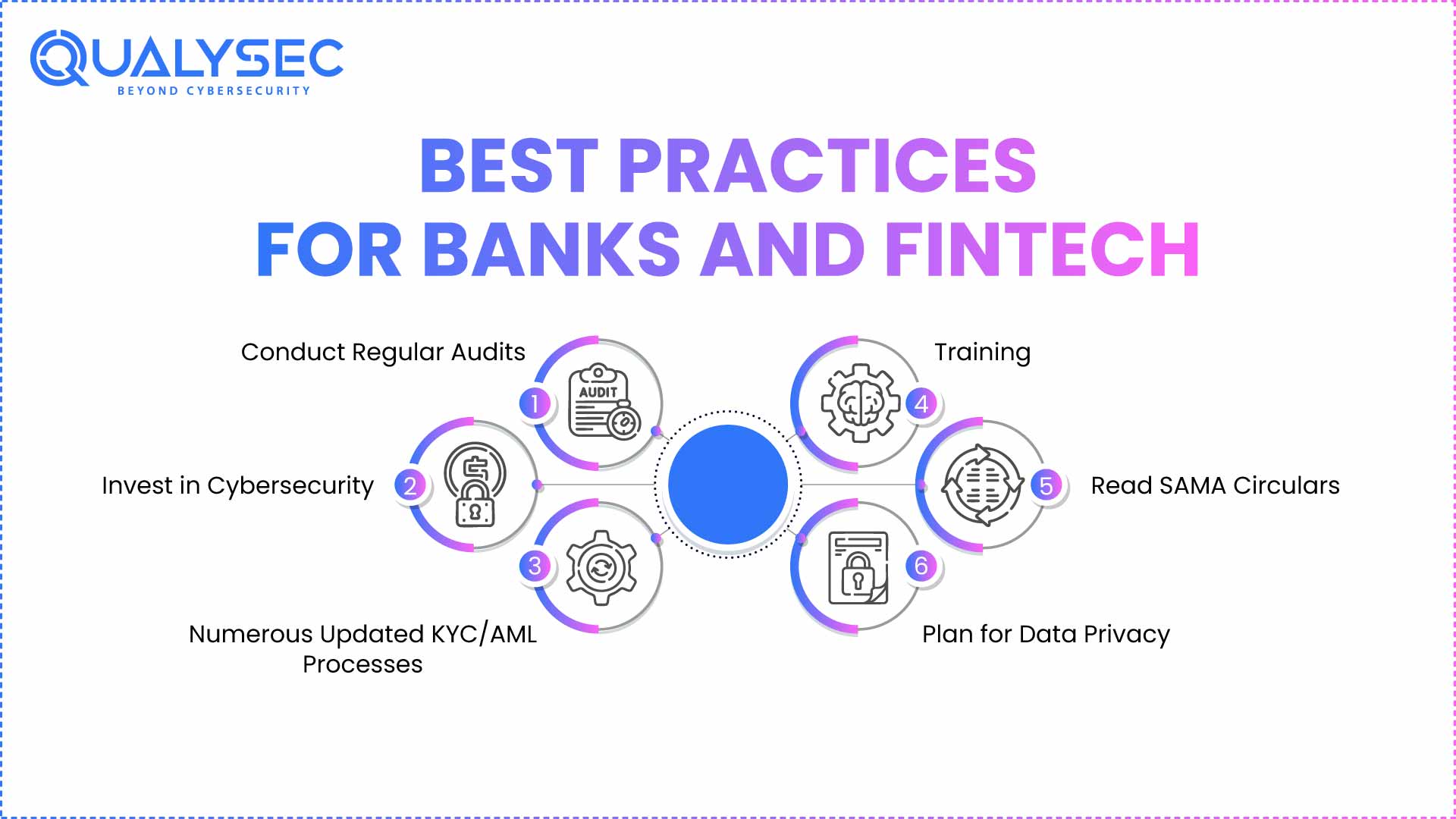

Best Practices for Banks and FinTech

Staying compliant with SAMA doesn’t need to be complicated if you follow the right steps. Here are some proven best practices:

1. Conduct Regular Audits

You should be conducting internal audits yourself or hiring a third-party auditor to help catch compliance issues before SAMA notices. Learn more on compliance security audit.

2. Invest in Cybersecurity

Have good secure development practices, have multi-factor authentication (MFA), and conduct penetration tests on a regular basis.

3. Numerous Updated KYC/AML Processes

Automate identity checks and transaction monitoring to remain compliant with SAMA’s anti-money laundering requirements.

4. Training

Educate your staff on compliance basics, handling data, and cyber threat responses.

5. Read SAMA Circulars

Keep abreast of all regulatory notices – you may want to assign one person or team to know when SAMA changes something.

6. Plan for Data Privacy

Plan and orient yourselves with SAMA rules and SDAIA legislation to ensure customer data is managed lawfully, safely, and transparently.

Each of the steps outlined above can help you build trust, avoid penalties, and set your business up for a successful future, as the financial sector in Saudi Arabia continues to grow.

Learn how banks can stay protected with Cybersecurity in Banking

How Can Qualysec Help?

Qualysec is a global cybersecurity and compliance company that specialises in supporting banks and fintechs in achieving complex standards such as SAMA’s framework. With considerable experience in the Saudi market, we know exactly what local regulators expect and how to help companies maintain compliance and stay secure.

We have Vulnerability Assessment and Penetration Testing (VAPT) to check what security issues your systems, apps, and networks may have. Our compliance consulting services are a way to cut through the SAMA framework and easily apply the rules and regulations in a pragmatic way, and save you time with our free, ready-to-use documentation templates, including cybersecurity policies and audit checklists.

Qualysec gives employee awareness programs training to your workforce so they know how to identify potential threats and follow compliance rules. More importantly, we provide ongoing support– audits and fixes (where required) to ensure you are prepared for inspections and updates.

Need help with SAMA compliance? Qualysec can guide you step-by-step.

Talk to our Cybersecurity Expert to discuss your specific needs and how we can help your business.

Conclusion

Saudi Arabia’s financial sector is growing quickly, and SAMA compliance is essential for building trust in the market and remaining secure. For banks and fintechs, compliance isn’t just compliance; it’s the backbone of a long-term, successful business.

Regardless of whether it’s getting the right license or compliance in cybersecurity, AML, KYC, etc., it’s imperative to nail compliance from the outset. While it may seem complicated, you can navigate these challenges and remain compliant with support from Qualysec. If you’re diversifying or launching in Saudi Arabia, now is the time to start policy writing and procedural documentation.

Get expert help with documentation, policies, and audits — choose Qualysec.

FAQ’s

1. What is the Complete Form of SAMA compliance?

SAMA compliance refers to all rules and standards that are followed by banks and fintechs in the Kingdom and are promulgated by SAMA.

2. What is the SAMA regulatory compliance?

SAMA regulatory compliance is to ensure that your business has met the legal, technical, and security requirements set by SAMA to operate in Saudi Arabia.

3. What does the SAMA stand for?

SAMA is short for the Saudi Arabian Monetary Authority, serving as Saudi Arabia’s central bank and financial overseer.

4. What is the SAMA regulation?

SAMA’s regulations comprise laws related to financial companies’ licensing, cybersecurity, data confidentiality, measures against money laundering, and customer safeguarding.

5. What is SAMA compliance in Saudi Arabia?

In Saudi Arabia, SAMA compliance means that your bank or fintech operates lawfully and securely as it adheres to SAMA’s standards.

6. What is the SAMA in Saudi Arabia?

SAMA is Saudi Arabia’s central bank that looks after the financial sector and aims for stability. It is in charge of consumer protection in Saudi Arabia and follows rigorous compliance standards.