Did you know that card fraud losses in the UK amounted to £572.6 million in 2024, as per UK Finance’s Annual Fraud Report 2024? The numbers are indeed staggering; however, it should not be forgotten that the majority of these breaches were due to companies that were unable to keep customers’ data safe. This is the main reason the PCI security standards were established.

The Payment Card Industry Data Security Standard (PCI DSS) is a universal standard that defines the minimum security measures required to protect cardholder data in any part of the world at every stage of its lifecycle: processing, storage, or transmission.

In this blog, we explain what PCI DSS really means, who must comply, what the standard requires, and how Qualysec helps businesses achieve PCI DSS compliance.

What Are PCI Security Standards?

The PCI DSS, or the Payment Card Industry Data Security Standard, is a framework that offers security for cardholder data. It protects data in processing, storage, and transmission.

The PCI DSS outlines both the technical and the operational practices that organizations must adopt in order to protect sensitive payment data. The measures comprise firewalls, secure transmission, access control management, network testing, and the application of security policies for the information involved. Knowing the PCI requirements helps businesses achieve PCI compliance certification easily.

Schedule Your PCI Gap Assessment Today!

Who Needs to Comply in the UK?

Any business dealing with the storage or processing of cardholder data has to adhere to the PCI DSS standards.

The list of such organizations includes:

- Merchants – Consisting of retailers, hospitality operators, online shops, or service providers, anybody accepting debit or credit cards counts as a merchant.

- Payment processors and gateways – The transactions are handled by these entities that route, authorize, or settle them.

- Third-party service providers – Cloud hosts, managed IT providers, or developers that manage systems touching payment data.

You might like to read about Achieving PCI DSS Compliance in Cloud Environments.

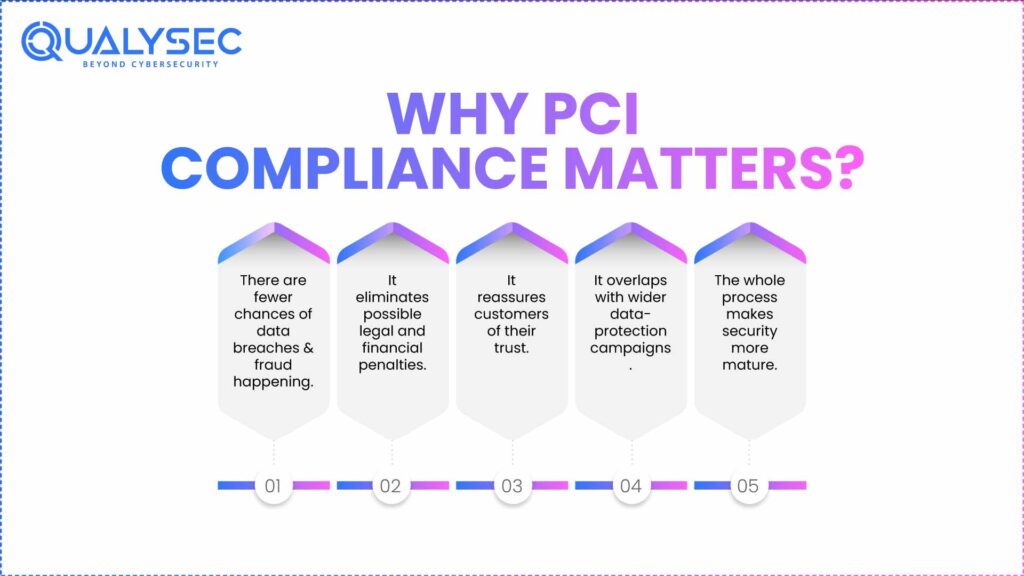

Why PCI Compliance Matters?

PCI DSS compliance is more than a tick-box requirement; it’s a baseline for digital trust and operational resilience.

1. There are fewer chances of data breaches and fraud happening.

The PCI DSS has across-the-board security measures, which include encryption, management of vulnerabilities, strong access controls, and network monitoring. This blocks the majority of attack pathways that are commonly used in card-skimming and malware campaigns.

2. It eliminates possible legal and financial penalties.

The card brands can impose fines on acquiring banks when merchants are non-compliant, and those costs usually trickle down to merchants. Non-compliance may result in extra fees or monthly fines of about £4,000 to £80,000, depending on the acquirer’s policy and the impact of the breach. Learn more about PCI Compliance Cost.

3. It reassures customers of their trust.

British consumers are less and less trusting of companies’ practices regarding their payment data. Proving PCI compliance test is a way of showing that your company applies the same accepted standards as everyone else, and not relying on security measures that are not tested.

4. It overlaps with wider data-protection campaigns.

Several PCI DSS principles, including access control, data minimisation, and encryption, are identical to those set by EU GDPR. Operating under one of the two governs your compliance with the other.

5. The whole process makes security more mature.

The audits, vulnerability scans, and documented policies required by PCI DSS often expose bigger IT weaknesses that can then be dealt with before they turn into expensive incidents.

Contact Us to Start Your PCI Compliance Journey Today!

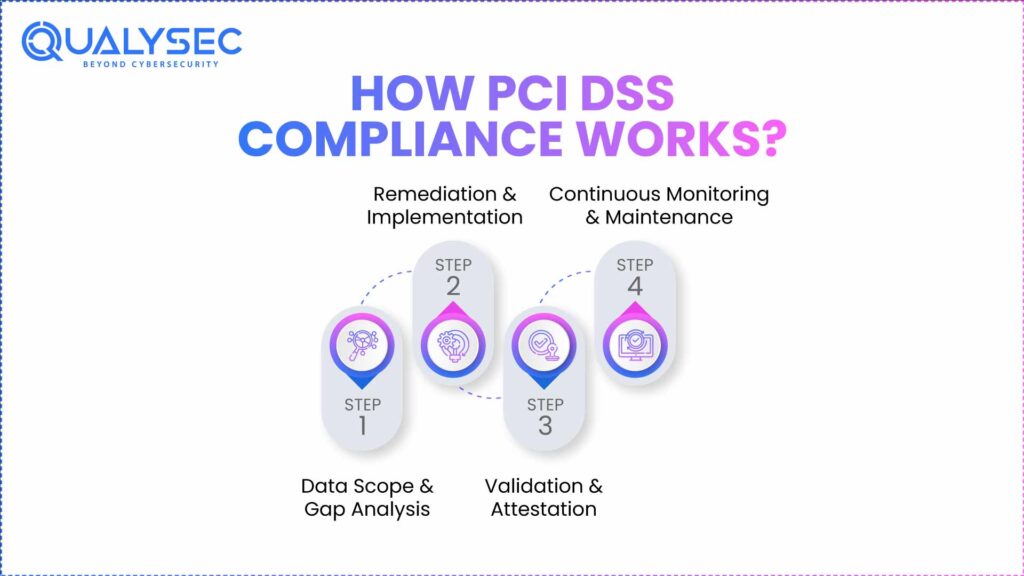

How PCI DSS Compliance Works?

Here is a step-by-step breakdown of how PCI DSS compliance works –

Step 1 – Data Scope and Gap Analysis

Identify where cardholder data is; this should encompass any system or service that is involved in storing, processing, or transmitting card data. A gap assessment must be done to understand which PCI controls are already in place and what gaps need to be fixed.

Step 2 – Remediation and Implementation

Fill in the gaps by employing security practices like patch management, firewalls, encryption, multi-factor authentication, and access reviews.

At this point, a lot of companies will get the help of independent testers like Qualysec to do PCI-aligned penetration tests or vulnerability scans that will be their way of validating the changes made.

Step 3 – Validation and Attestation

This will depend on your merchant level:

- Level 1 has to go through an annual on-site audit by a Qualified Security Assessor (QSA).

- Levels 2-4 usually fill out a Self-Assessment Questionnaire (SAQ) and submit an Attestation of Compliance (AOC) to their acquirer with the questionnaire.

Step 4 – Continuous Monitoring and Maintenance

PCI DSS poses requirements with ongoing activities such as:

- Conducting quarterly vulnerability scans and annual penetration testing (Requirement 11).

- Monitoring logs and access controls (Requirement 10).

- Updating policies and training staff (Requirement 12).

See What Makes Our Clients Trust Us — View Our Case Studies.

Common Pitfalls and How to Avoid Them

Sometimes, even the best companies may lose their compliance status or fail their audits due to small mistakes. Here’s a list of the most common PCI DSS errors and what to do to steer clear of them.

1. Poor scoping

Very often, companies misunderstand the size of the CDE; they either include too many elements or miss an important system altogether.

Solution: Team up with your acquirer or security provider to pinpoint every single network, database, or API that is involved in processing or transmitting cardholder data. Apply PCI DSS segmentation testing to validate the separation between the systems that are in scope and those that are out of scope.

2. Over-reliance on third-party processors

Using payment gateways such as Stripe, Square, or Worldpay has the effect of lessening exposure; however, it does not relieve the entity of its compliance responsibilities.

Solution: Make certain that your integrations, plugins, and redirections conform to the PCI-approved setup of the processor. You will still be responsible for keeping customer data secure on your website or app before it reaches the payment gateway.

3. Weak documentation and evidence

Auditors and acquiring banks require proof, not promises. It is for this reason that performing a PCI Risk Assessment is crucial, as it not only showcases the organization’s compliance but also fortifies the security of the data.

Solution: Keep records of scans, remediation reports, and change-management logs. If you fix vulnerabilities, keep dated evidence showing when and how the issue was resolved.

4. Untrained or unaware staff

Many breaches start with avoidable human error, such as storing card data in spreadsheets or emailing customer details.

Solution: Provide clear internal guidance. PCI DSS Requirement 12 specifically mandates employee security awareness and defined responsibilities.

Download the PCI DSS Penetration Testing Report. Discover key insights to strengthen your payment data security.

How Qualysec Helps You Stay Compliant?

At Qualysec, our role is to help businesses test, validate, and evidence their PCI security controls accurately and transparently. Our professionals perform network, web apps, APIs, and cloud systems real-world testing in order to check the PCI cloud compliance with Requirement 11 and the segmentation integrity. Furthermore, we also give practical suggestions and retest the system that has been fixed in order to make sure that vulnerabilities have been completely shut down.

Conclusion

Card data breaches don’t just cause financial loss. They damage trust, reputation, and payment privileges. That is the very reason for the existence of the PCI Security Standards. It guarantees that every business that comes into contact with payment data implements the same high-assurance security framework.

Qualysec assists businesses in transforming the PCI DSS from a complicated framework into a systematic and achievable process. We walk you through the entire process, starting from gap assessments, going through PCI pentest, and ending with remediation validation.

Speak with our PCI compliance specialist today!

FAQs

1. What are the PCI security standards?

The Payment Card Industry Data Security Standard (PCI DSS) is an international standard that describes the essential and minimal secure way of storing, processing, and transmitting cardholder data and making it impossible for anyone without the necessary authorization to access it.

2. What are the 4 levels of PCI compliance?

PCI DSS defines four merchant levels based on annual transaction volume:

- Level 1: Over 6 million – requires a QSA audit.

- Level 2: 1 – 6 million – SAQ + quarterly ASV scans.

- Level 3: 20,000 – 1 million – SAQ + quarterly scans.

- Level 4: Under 20,000 – SAQ + bank-directed validation.

3. What does PCI stand for?

PCI refers to the Payment Card Industry, the group that enforces the global security of how to handle cardholder data.

4. Is PCI DSS mandatory in the UK?

In the UK, the government does not impose PCI DSS as a law. All merchants and service providers that deal with card data must validate compliance, as acquiring banks and card networks set this requirement.

5. What is PCI DSS certification?

The PCI DSS certification (technically referred to as the Attestation of Compliance) serves as a formal statement that the organization has complied with the requirements validated either by a Qualified Security Assessor (QSA) or by using the appropriate Self-Assessment Questionnaire (SAQ).

Have any questions? Feel free to ask now—our cybersecurity experts are here to help.