Your payment information passes through several systems before landing at the bank whenever you pay with your card, whether online or in a physical store. Hackers are waiting at every level to grab that information. Then what secures it? The solution rests in the 12 PCI DSS Compliance Requirements, a framework created to safeguard confidential cardholder data.

PCI DSS compliance, however, for many companies seems like a labyrinth of audits, rules, and technological measures. One can get consumed in the specifics and find oneself swamped. That’s what led us to write this tutorial. You will find the PCI DSS compliance criteria spelt out in simple language here, along with the PCI DSS compliance checklist and a step-by-step procedure to get certified. This breakdown will help you protect client trust and prevent expensive fines, whether you run a developing internet shop or a multinational company.

Ready to make compliance simple? Let’s dive in!

What does PCI DSS compliance mean?

PCI DSS (Payment Card Industry Data Security Standard) is a set of widely known security measures meant to protect cardholder data. It applies to any company, small or large, that saves, uses, or passes credit card details. Therefore, should you take card payments in any way, you should meet these PCI DSS Compliance Requirements.

Created by major card companies like Visa, Mastercard, American Express, Discover, and JCB, the PCI Security Standards Council (PCI SSC) sets this standard. Its primary goals include decreasing card fraud, preventing data breaches, and giving clients confidence while purchasing.

Compliance, essentially, is not elective. Failing to abide by the PCI DSS standards can lead to legal proceedings, fines, and even loss of the ability to accept card payments. That’s why PCI DSS should be regarded as more than just a rule; rather, it’s a cornerstone of digital trust by any serious company prioritizing customer trust.

Why PCI DSS Compliance Matters Globally

1. Protects customers from fraud

PCI DSS shields against data stealing. Using robust encryption, access restrictions, and monitoring, companies can guarantee that consumer data does not end up in the wrong hands.

2. Helps businesses avoid penalties

Non-compliance is costly. Fines can range up to $500,000 per event, depending on the degree of a breach. Moreover, businesses might be sued and suffer reputational harm, from which recovery takes years.

3. Builds long-term customer trust

Consumers are growing more security aware. They want a guarantee that their financial and personal information is secure. Your company considers security seriously, as PCI DSS requirements show, which might directly increase consumer loyalty.

4. Aligns businesses with global standards

PCI DSS compliance is respected whether you work across nations or locally. Following it helps you stay competitive in a digital-first world, obtain world clients, and cooperate with foreign payment processors.

If you’re aiming for global growth, compliance isn’t just a requirement—it’s your competitive advantage!

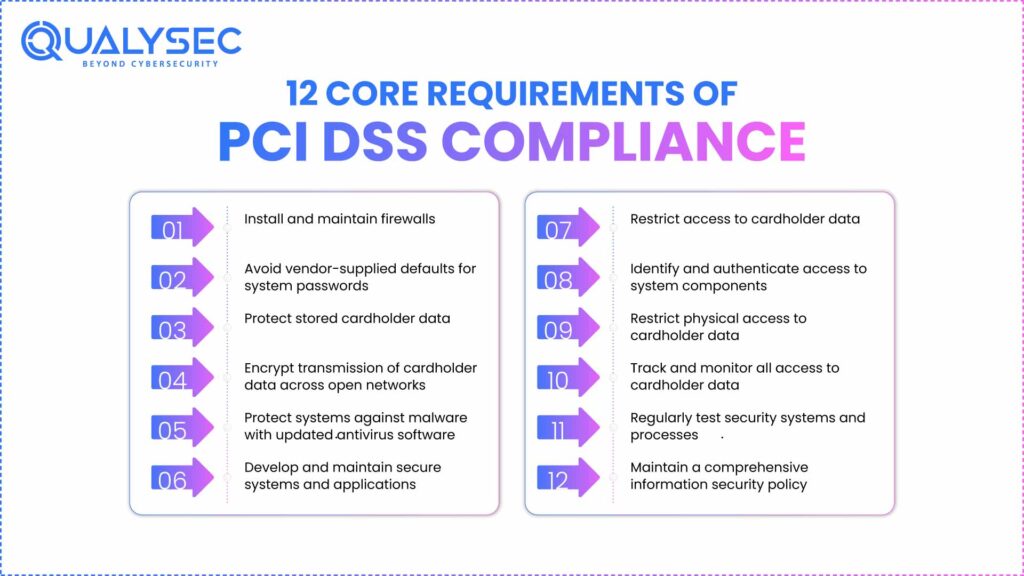

The 12 PCI DSS Compliance Requirements

The 12 PCI DSS compliance requirements are split into six guiding principles, one addressing each of the six dimensions of payment security. They create a strong architecture together that considers both physical and digital weaknesses.

Principle 1: Build and Maintain a Secure Network and Systems

Requirement 1: Install and maintain firewalls

Acting as digital gatekeepers, firewalls allow legitimate transactions while denying unauthorised access. Companies have to set up firewalls for internal as well as external networks, so as to avoid any gaps. Stopping cybercriminals before they reach sensitive information depends on this initial layer of defence.

Requirement 2: Avoid vendor-supplied defaults for system passwords

Many organisations fail to change default user names and passwords on servers, routers, or software. Hackers are quite familiar with these defaults and may quickly use them. Businesses must employ distinctive, secure passwords across all systems to close this basic but serious flaw to meet PCI DSS security requirements.

Principle 2: Protect Cardholder Data

Requirement 3: Protect stored cardholder data

Always encrypt sensitive information kept—that is, names, account numbers, or expiration dates. Some data, including CVV codes and PINs, should never be recorded in any manner. This decreases the possibility of significant breaches whereby hackers have access to consumer databases.

Requirement 4: Encrypt transmission of cardholder data across open networks

Data sent through the internet becomes interception-friendly. PCI DSS requirements strong encryption methods, including IPsec, VPNs, or TLS. This assures that taken cardholder information taken will be unreadable. Virtual payment gateways and e-commerce sites especially need safe communication.

Read more: Ecommerce Security – How to Prevent Cyberattacks

Principle 3: Maintain a Vulnerability Management Program

Requirement 5: Protect systems against malware with updated antivirus software

Cybercriminals are continuously creating fresh malware meant to steal or compromise information. Every company’s systems have to have anti-malware, anti-spyware, and anti-virus software per PCI DSS. Their continued currentness is just as crucial for their ability to identify and counteract new hazards.

Requirement 6: Develop and maintain secure systems and applications

Attacks may simply enter through flaws in legacy systems or poorly constructed applications. Following safe development methods and regular security updates helps companies to avoid SQL injection or cross-site scripting attacks. Being proactive with patch management eliminates the need for any negotiating.

Principle 4: Implement Strong Access Control Measures

Requirement 7: Restrict access to cardholder data

Everybody should not have access to covert knowledge. Only need-to-know access should be provided. Organizations use role-based access control (RBAC) to lower the likelihood of insider threats and inadvertent disclosure.

Requirement 8: Identify and authenticate access to system components

Cybersecurity is a continual process, not a one-off setup. PCI DSS security requirements require penetration tests and vulnerability scans as continuous testing. These tests expose vulnerabilities before attackers might exploit them by reproducing real attacks. Regular testing lets your defenses grow along with emerging threats.

Requirement 9: Restrict physical access to cardholder data

Digital security is inadequate if physical security is poor. Physical protection of servers, payment terminals, and storage devices containing cardholder information is essential. Using access badges, locks, or surveillance cameras, only authorized people should be given limited access.

Principle 5: Regularly Monitor and Test Networks

Requirement 10: Track and monitor all access to cardholder data

Every time someone accesses systems managing cardholder data, that action should be recorded. Audit logs allow one to follow doubtful behavior back to its origin. PCI DSS mandates that companies keep these records for at least a year to help examine breaches that may arise.

Requirement 11: Regularly test security systems and processes

Cybersecurity is an ongoing process rather than a one-time installation. PCI DSS security requirements require ongoing testing, including vulnerability scans and penetration tests. Before attackers could abuse them, these tests reveal flaws by means of simulated actual attacks. Your defenses can develop with new hazards thanks to constant testing.

Principle 6: Maintain an Information Security Policy

Requirement 12: Maintain a comprehensive information security policy

The last requirement guarantees workers and contractors know their role in safeguarding data. An effective policy defines permissible use, security obligations, and incident response procedures. Regular staff training helps to avoid human mistakes, the most frequent cause of breaches.

Compliance starts with people as much as technology. Investing in awareness training is just as important as deploying firewalls!

PCI DSS Compliance Checklist

1. Map and document your cardholder data flow across systems

The first step in safeguarding cardholder information is knowledge of the path it follows throughout your surroundings. Follow the path from the place of collection—an online checkout or payment terminal, for example—through every system where it is sent, processed, or saved. Recording this flow provides visibility into possible vulnerabilities attackers might exploit. Additionally, it clarifies the scope of your PCI DSS Compliance Requirements and guarantees no system is neglected.

2. Set firewalls and encryption for all sensitive information

By filtering doubtful traffic, firewalls distinguish reliable internal networks from external networks. Conversely, encryption transforms cardholder information into an undecipherable code, thereby making it useless to attackers even if intercepted. Together, these protections offer a sturdy barrier for inactive data as well as data in transit.

3. Use unique, powerful passwords in place of all vendor default credentials.

Hackers often aim at well-known default usernames and passwords included with software or tools. Replacing them with real, distinctive credentials greatly reduces the chance of unauthorized access. Long, complicated passwords need to be updated frequently. Employing this tactic across all systems improves the security stance against brute force attacks and credential stuffing.

4. Install and update antivirus and anti-malware solutions.

Anti-malware and antivirus solutions let you find and delete hazardous software that could endanger your computer. These utilities track traffic and files in order to prevent dangers from doing any damage. Since new malware and infections keep emerging, regular updates are vital. Maintaining your defenses helps to safeguard your environment from both emerging and daily hazards.

5. Keep secure coding techniques and patch programs.

Unpatched software creates security holes that attackers can exploit. Timely deployment of patches and updates closes these gaps and boosts general resilience. Developers should adhere to safe coding standards for in-house built systems, including error handling and input validation.

6. Limit data access by job roles only.

Not every employee requires cardholder data to do their job. Restricting access depending on the employment role guarantees sensitive information is only accessible to those who really need it. This least privilege approach lowers the possibility of purposeful abuse as well as inadvertent data disclosure. Using role-based permissions also greatly simplifies access auditing and monitoring.

7. Set up multi-factor authentication for system login.

By demanding consumers confirm their identities with more than only a password, multi-factor authentication (MFA) enhances security. This may be a hardware token, a fingerprint scan, or a code sent to a mobile device. MFA makes it very difficult for attackers to get in, even if a password is taken. One of the most successful strategies to stop unwanted access is to add this extra layer of protection.

8. Physical data storage, payment terminals, and secure servers

If physical systems are still open, cybersecurity measures are insufficient. Payment systems should be tamper-proof, servers should be kept in locked rooms, and physical storage holding sensitive information should be locked. Equipment that processes or saves cardholder data should never be easily available to unauthorized people. Good physical security lowers the possibility of stealing, damage, or tampering with vital assets.

9. Activate logging and keep audit logs for at least a year.

Tracking who viewed data, when, and from where depends on system and access logs. Organizations create a trustworthy trail by turning on logging that can be studied in the event of a security breach. Storing these logs for at least one year is PCI DSS’s demand; the most recent three months must be readily reviewed. Reporting on compliance and investigations also depends on these logs.

10. Frequently conduct penetration tests and vulnerability checks.

Regular checks find security issues before criminals can capitalise on them. Although PCI DSS penetration tests reveal hidden flaws via simulated real attacks, vulnerability scans automatically flag unpatched systems or misconfigurations. Regular reviews help to maintain the strength and worth of your defenses. This proactive strategy supports continuous compliance and helps to avoid misdeeds.

11. Archive a thorough security policy and modify it in accordance with developing threats.

A short, written security policy outlines the standards for cardholder data management. It should include something from access control to incident response. Policies should be updated and reviewed to stay current with the development of new dangers. Maintaining this document currently lets stakeholders and the government know that your company is dedicated to data security and compliance.

12. Provide training in security awareness for all contractors and employees

Usually, employees constitute the weakest link in the chain of security. They master strong passwords, detect phishing attacks, and correctly manage sensitive data. Regular meetings promote positive behaviors and lower hazardous ones that might reveal secrets.

0 Comments